Introduction to Credit Default Swaps

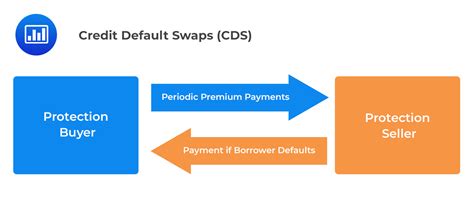

Credit default swaps (CDS) are financial instruments that have gained significant attention in recent years due to their role in managing and transferring credit risk. A CDS is essentially an insurance contract between two parties, where one party purchases protection against default by a third party (the reference entity) for a defined period of time. In exchange for this protection, the buyer of the CDS makes periodic payments to the seller. If the reference entity defaults, the seller of the CDS pays the buyer the face value of the debt in exchange for the physical securities. Understanding CDS is crucial for investors, financial institutions, and corporations seeking to hedge against credit risk.

How Credit Default Swaps Work

The mechanism of CDS involves a buyer and a seller. The buyer is seeking protection against the default of a reference entity, which could be a corporation, a sovereign government, or any other entity that issues debt. The seller of the CDS, on the other hand, is providing this protection. The terms of the contract define the reference entity, the credit events that trigger a payout (such as bankruptcy or failure to pay), the notional amount (the amount of protection bought), the duration of the contract, and the premium payments (the cost of the protection). The buyer pays the premium to the seller over the life of the contract. If no credit event occurs, the seller retains the premium payments as profit. However, if a credit event occurs, the seller must pay the buyer the face value of the contract in exchange for the reference entity’s debt obligations.

Benefits and Risks of Credit Default Swaps

CDS offer several benefits, including the ability to hedge against credit risk, to speculate on the creditworthiness of reference entities, and to gain exposure to credit markets without directly holding the underlying debt. However, they also come with significant risks. The buyer of a CDS is exposed to the risk that the seller may default on their obligations under the contract. Additionally, the value of a CDS can fluctuate significantly based on changes in the creditworthiness of the reference entity and market conditions. For the seller, the risk is potentially catastrophic if a credit event occurs, as they may be obligated to pay out a large sum.

5 Tips for Engaging with Credit Default Swaps

Engaging with CDS requires a deep understanding of the financial markets, the reference entities involved, and the terms of the CDS contracts. Here are five tips for those considering CDS: - Conduct Thorough Research: Before buying or selling a CDS, it’s crucial to conduct thorough research on the reference entity. This includes analyzing their financial health, credit rating, industry trends, and any potential risks or opportunities. - Understand the Contract Terms: The terms of a CDS contract are complex and include details such as the notional amount, the premium, the duration, and the conditions under which a payout will be made. Understanding these terms is essential for managing risk and potential returns. - Diversify Your Portfolio: Like any investment, it’s important to diversify when engaging with CDS. This can help manage risk by spreading investments across different reference entities and sectors. - Monitor Market Conditions: The value of a CDS and the likelihood of a credit event can be significantly influenced by market conditions. Staying informed about economic trends, regulatory changes, and other market factors is crucial. - Seek Professional Advice: Given the complexity and risk associated with CDS, seeking advice from a financial professional can be highly beneficial. They can provide insights into the best strategies for your specific situation and help navigate the complexities of CDS markets.

Best Practices for Managing Credit Default Swaps

Managing CDS effectively requires ongoing monitoring and a proactive approach to risk management. This includes: - Regularly reviewing the creditworthiness of the reference entities in your CDS portfolio. - Adjusting your portfolio as necessary to reflect changes in market conditions or the financial health of reference entities. - Maintaining a diversified portfolio to mitigate risk. - Staying up-to-date with regulatory requirements and market practices related to CDS.

| Reference Entity | Credit Rating | Premium | Notional Amount |

|---|---|---|---|

| Entity A | AAA | 1% | $10 million |

| Entity B | BBB | 3% | $5 million |

📝 Note: The information provided in the table is hypothetical and for illustrative purposes only. Actual data may vary based on market conditions and the specific terms of CDS contracts.

In conclusion, credit default swaps are complex financial instruments that can be powerful tools for managing credit risk, but they also come with significant risks and require a deep understanding of the underlying markets and contract terms. By following the tips outlined above and adopting best practices for managing CDS, investors and financial institutions can navigate these markets more effectively.

What is the primary purpose of a credit default swap?

+

The primary purpose of a credit default swap is to transfer credit risk from one party to another, providing protection against default by a reference entity.

What are the key components of a CDS contract?

+

The key components include the reference entity, credit events, notional amount, duration, and premium payments.

Why is diversification important when engaging with CDS?

+

Diversification is important because it helps manage risk by spreading investments across different reference entities and sectors, reducing the impact of any single credit event.